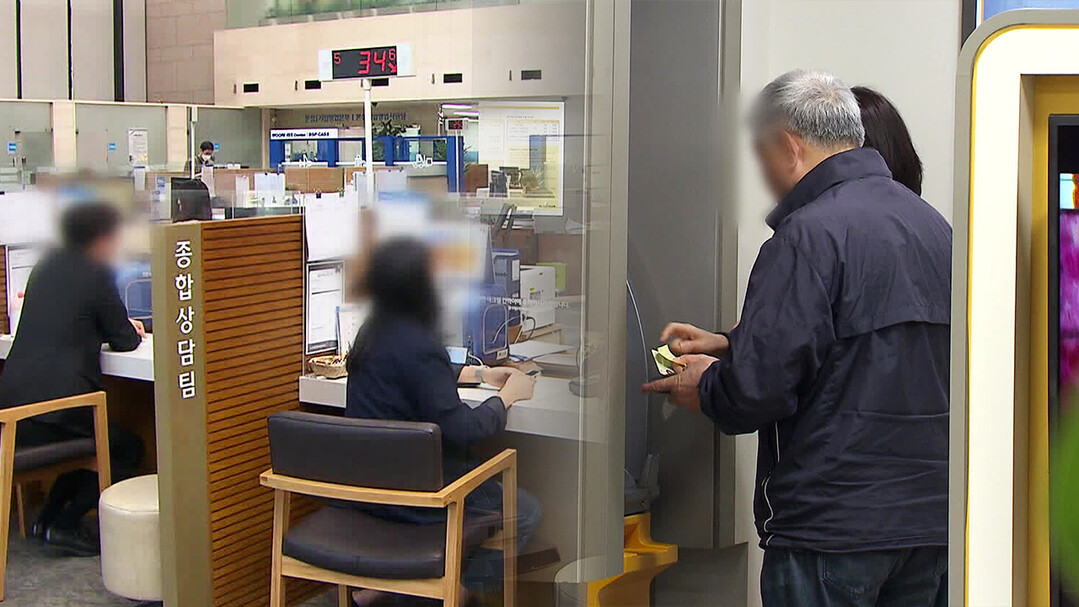

Banks are rapidly reducing the number of their physical branches to improve efficiency by cutting costs and strengthening their non-face-to-face service capabilities. This trend raises concerns about the potential exclusion of vulnerable groups, such as the elderly, from financial services. While banks are offering solutions like financial education for seniors and user-friendly mobile apps, some argue that more fundamental measures are needed to address the core issue.

KB Kookmin Bank, for example, is set to close 28 branches next month, following the lead of other major banks in South Korea. The total number of branches operated by the top five domestic banks has decreased by 3.5% in the past year, reaching 3,790 as of the end of last year. This decline is attributed to the rise in non-face-to-face transactions via smartphones and other digital devices, which has led to a sharp decrease in in-person transactions at bank branches.

According to the Bank of Korea, in the third quarter of last year, the proportion of in-person transactions among banking services was at an all-time low of 3.6%. The proportion of in-person inquiries was also only 4.8%. Even loan services are increasingly being handled remotely. At Hana Bank, for instance, the proportion of non-face-to-face mortgage loans and unsecured loans last year was 74.3% and 94.2%, respectively.

In response to concerns about the potential isolation of vulnerable groups, banks are implementing various measures. Woori Bank has established 'WOORI Senior IT Happy Learning Centers' in senior welfare facilities, providing education on using the latest digital devices and practicing kiosk operation. Hana Bank, in partnership with the Ministry of Education, is conducting digital financial literacy education for senior citizens. Shinhan Bank also opened 'Hagijae', a senior financial education center, in Namdong-gu, Incheon last year.

However, some argue that these measures are insufficient. Many seniors still experience difficulties with non-face-to-face transactions, even after receiving education. Therefore, more fundamental solutions are needed to ensure that customer inconvenience is fully addressed.

One financial industry representative suggested that banks should acknowledge the limitations of digitalization and consider alternative solutions, such as allowing post offices across the country to handle banking services for rural and elderly customers. This would require legislative amendments to financial regulations to prevent system crashes and other potential issues.

In conclusion, while banks are striving to improve efficiency through branch closures and digitalization, it is crucial to find a balance between these goals and the needs of vulnerable groups. More comprehensive and practical solutions are needed to ensure that everyone has access to essential financial services.

[Copyright (c) Global Economic Times. All Rights Reserved.]